How a campaign quietly rewrote the ritual of engagement.

A few months ago, I hosted a small get-together for a few colleagues and their families. As the evening went on, conversations drifted into smaller groups. At one point, my wife and the wife of one of my colleagues were comparing the gifts they had received from their husbands over the years. When my wife showed her bracelet, the first reaction came almost instantly.

“Are these real diamonds?”

The question was not unusual. If anything, it felt like the most natural thing to ask. The bracelet was passed around for a closer look, and the conversation moved briefly into the familiar territory of carats, clarity, and where it had been purchased. What struck me later was not the curiosity about the bracelet itself, but the assumption behind the question. The value of the piece was being measured through one specific lens: whether the stones were diamonds. It felt normal because it has become normal.

Across much of the world today, diamonds occupy a peculiar place in the social imagination. They are not merely gemstones. They function as shorthand for authenticity, seriousness, and permanence. Engagements, anniversaries, and milestones often appear incomplete without them. The strange part is how recent this expectation actually is.

Barely a century ago, diamonds were not the default choice for engagement rings in the United States or in many parts of Europe. Jewelers regularly sold rings set with sapphires, emeralds, or simple gold bands. Diamonds were admired, certainly, but they were not yet the universal language of romantic commitment. The transformation of diamonds into that symbol did not occur through centuries of tradition. It emerged from a far more deliberate process—one that began when a company confronting a structural market problem decided to change not the product itself, but the meaning attached to it.

The company at the center of this shift was De Beers, the firm that by the early twentieth century controlled the majority of the world’s diamond supply through mining concessions, exclusive agreements, and a distribution system that functioned, in practice, as a global cartel. At first glance diamonds should have been an ideal commodity: durable, visually striking, and geologically scarce. Those same qualities, however, produced an unusual economic dilemma.

Diamonds do not wear out. Unlike gold that can be melted down or fashions that eventually disappear, diamonds remain in circulation indefinitely. Once purchased, they tend to pass quietly from one generation to the next. In practical terms this meant that every diamond ever mined continued to exist somewhere in the market. Over time the accumulated supply would grow larger regardless of current production.

By the 1930s this structural reality became difficult to ignore. The Great Depression had sharply reduced disposable income, and demand for luxury goods had weakened across the United States, one of the industry’s most important consumer markets. Sales were falling at precisely the moment when the long-term stock of diamonds in circulation continued to expand.

For a firm whose economic model depended on selling newly mined stones, the risk was existential. Cutting prices might have moved inventory in the short term, but doing so would have undermined the perception of rarity on which diamond value depended. If prices fell too far, diamonds risked drifting into the category of ordinary luxury goods—beautiful perhaps, but ultimately interchangeable with other gemstones.

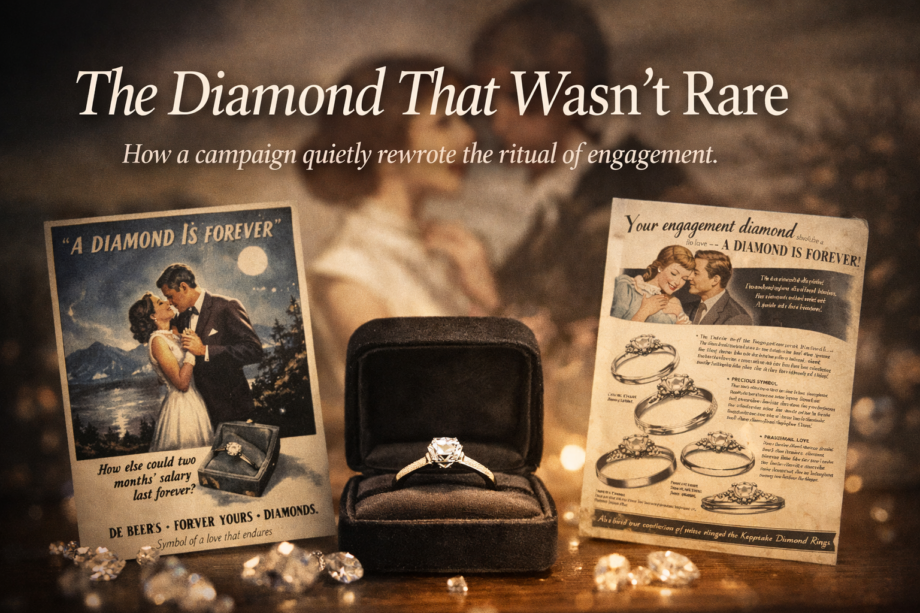

The response would not come through conventional promotion. Instead, De Beers sought to reshape the cultural meaning surrounding the product itself. In 1938 the company turned to the New York agency N.W. Ayer with a brief that was unusual in its ambition: increase demand for diamonds by embedding them within the rituals of modern romance.

The strategy that emerged extended far beyond conventional advertising. If diamonds were to become culturally indispensable, they could not appear as products being promoted. They had to appear as the natural expression of commitment itself. Hollywood films began featuring diamond engagement rings in pivotal romantic scenes. Fashion magazines highlighted the rings worn by actresses and socialites. Newspaper engagement announcements increasingly referenced the size and quality of the stones involved. Through repeated exposure across these cultural channels, the association between romance and diamonds slowly settled into public imagination.

The effort reached beyond the entertainment industry. Educational materials describing the symbolism and history of diamonds circulated in schools, and lectures on courtship and marriage quietly reinforced the idea that a diamond engagement ring represented the appropriate expression of commitment. Over time the association became familiar enough that it no longer felt like persuasion.

During the 1940s the campaign introduced another element that would prove equally influential. Advertisements began suggesting that an engagement ring should represent a meaningful financial investment, initially implying that a man ought to spend roughly one month’s salary on the purchase. The guideline later evolved into the widely known “two months’ salary” rule. The recommendation had little connection to the intrinsic value of the stone. Its function was symbolic. The cost itself became a visible signal of seriousness.

In 1947, a young copywriter at N.W. Ayer, Frances Gerety, wrote a line that would eventually define the narrative framework surrounding diamonds: “A Diamond Is Forever.” The phrase accomplished several things simultaneously. It aligned the gemstone with the idea of enduring commitment, discouraged resale by implying the stone should never be relinquished, and reinforced the perception that diamonds were timeless objects rather than market commodities.

Seen from a distance, the transformation appears almost effortless. Within a few decades diamonds moved from being one gemstone among many to becoming the dominant symbol of engagement across much of the Western world. The scale of the shift becomes clearer when viewed through economic data. In 1939 De Beers’ wholesale diamond sales in the United States stood at $23 million. By 1979 they had reached $2.1 billion, an increase of nearly ninety-fold. The proportion of first-time brides receiving diamond engagement rings rose from roughly 10 per cent in 1940 to around 80 per cent by 1990.

Early results appeared quickly. Retail diamond sales rose about 25 per cent within the first six months of the campaign and increased roughly 55 per cent by 1941. These changes were not simply the result of evolving consumer taste. Other gemstones remained widely available throughout the same period, often at lower prices. Sapphires, emeralds, and rubies continued to exist within the jewelry market but never achieved comparable ritual status. Industry reports throughout the late twentieth century consistently showed diamonds accounting for the overwhelming majority of engagement rings in the United States, while coloured stones rarely exceeded a small share of the category.

The difference was not geological scarcity or aesthetic preference. It was narrative alignment. Only one gemstone had been systematically tied to a specific and repeatable social moment.

Had De Beers responded to the Depression merely by lowering prices, the diamond market might have followed a different path. Precious metals such as silver have often oscillated between luxury good and industrial commodity, their value shaped largely by fluctuations in supply and investment demand. Diamonds risked drifting toward a similar fate, becoming another beautiful but interchangeable luxury product whose price was determined by resale supply rather than cultural meaning.

Instead, by linking diamonds to the ritual of engagement, the industry shifted the economic structure of the market itself. Each new proposal became not merely a jewelry purchase but a reaffirmation of a social expectation.

Once a product becomes embedded in a ritual, the logic of the purchase changes. Birthdays bring cakes and candles. National holidays bring particular foods and decorations. Weddings carry their own set of objects and gestures that feel incomplete when they are absent. In such moments, consumption becomes part of a shared script rather than an isolated transaction.

Over time the commercial origins of that script fade. What remains is the sense that this is simply how things have always been done.

Stories like this often leave behind an interesting illusion. Once a practice becomes embedded in everyday life, it begins to feel as though it must have emerged naturally. Traditions appear ancient even when they are relatively recent.

When my wife passed her bracelet around the room and someone asked whether the stones were real diamonds, the question did not feel unusual. It felt automatic. No one paused to consider why diamonds had become the standard against which other stones were measured.

The expectation had already settled into everyday conversation. What began as a response to oversupply and cartel economics had quietly become the measure of seriousness itself. A gemstone entered culture not by outperforming alternatives in the marketplace, but by becoming part of the moment.

Once that happened, the market no longer needed to explain the choice. Society did it on its behalf and continues to do so long after the original economic logic has faded from view.